Asula is a Bitcoin Company.

Our mission is to build the next generation of financial products centered around Bitcoin by developing systems that replace trust with verifiable software.

In this document we provide reasoning behind our mission. We give background for our focus on finance & bitcoin, and then discuss the broader product vision for Asula.

Why finance?

Blockchains provide the best infrastructure for building out the next generation of financial products. Here’s why:

Blockchains are fundamentally slow but verifiable computers. The “blockchain” itself acts as a database with a virtual machine that can run different programs (these programs determine how state in the database changes). Anyone can run a node for a blockchain to verify the correctness of transactions (i.e. the validity of state transitions) on the chain. Consensus algorithms allow parties running node software to come to an agreement about the correctness of sets of transactions. This replication aspect of a blockchain is what makes it verifiable but also what makes blockchains slow and expensive as computers.

Finance is the perfect application for blockchains because of the following reasons:

Most financial workloads are text which means they aren’t as expensive as videos or images. Naturally, if we are going to 100x costs for running a piece of computation, the final cost is more bearable if the initial cost is cheaper.

Financial applications are high leverage: a small piece of computation can be very important for all parties involved. For example, a transfer of $1,000,000 requires the same amount of computation as moving $1 but is far more important for the parties involved.

If users do have to pay higher costs for computation, they must get value out of this cost. By using blockchains, financial counterparties are able to remove a trusted-third party from their transactions. This reduces risk during the transaction and also reduces the risk that funds involved in a transaction are censored. There are other benefits like transparent, real-time audits, but the reduction of counterparty-risk is the most significant.

The nature of financial application we think blockchains are useful for are:

Exchanges

Lending Venues

Asset Issuance (tokenization)

Asset Transfer Protocols

Almost all of finance can be encapsulated into some combination of this above set of applications. So naturally, the end state for Asula is to build out each of these applications on a verifiable platform.

But getting there will take a lot of work. We are executing on this path today by building out a wallet and a lending protocol for bitcoin users.

Bitcoin will be the lynchpin both as an asset and as a network for the work that Asula does. We believe it has achieved the status of a Store of Value (SoV) and continues to grow as one of the largest assets in the world. We’ll talk more about how we use bitcoin the asset and the network below.

Why Bitcoin?

Currently there are two divergent views on blockchain design:

Integrated/Monolithic (a la Solana and Monad)

Modular (a la Ethereum, Celestia)

The integrated approach relies on optimizing software and upgrading hardware but generally maintains the shape of a traditional blockchain. The traditional shape involves a set of nodes that are part of the network. Every slot, a node is elected as the block producer. The block producer receives user transactions, orders them into a block and then broadcasts these transactions to the rest of the nodes on the blockchain. Each of these nodes then re-runs every transaction in the block to verify the transactions and then votes on the block’s validity. A consensus algorithm then tallies the votes and finalizes the block to progress the blockchain.

During the last few years we’ve seen Ethereum’s vision transform into a fully modular blockchain architecture. In this vision, offchain domains called L2 or rollups become central. The core piece of enabling technology here are zero-knowledge (ZK) proofs or validity proofs. As previously mentioned blockchains rely on repeated computation to verify transactions. But ZK proofs allow for the computation to be done once and verified everywhere. When using ZKPs, proofs are generated along with a computation. The verification of this proof is constant time irrespective of the computation involved, reducing the repeated load on the nodes of the system. While producing the proof itself is quite expensive today compared to vanilla computation, the costs have been reducing greatly over the last few years. If you want to read more on this, here is some related reading courtesy of research from our team over the last few months: Wtf is settlement and Consensus where it counts (both posts on Bedlam).

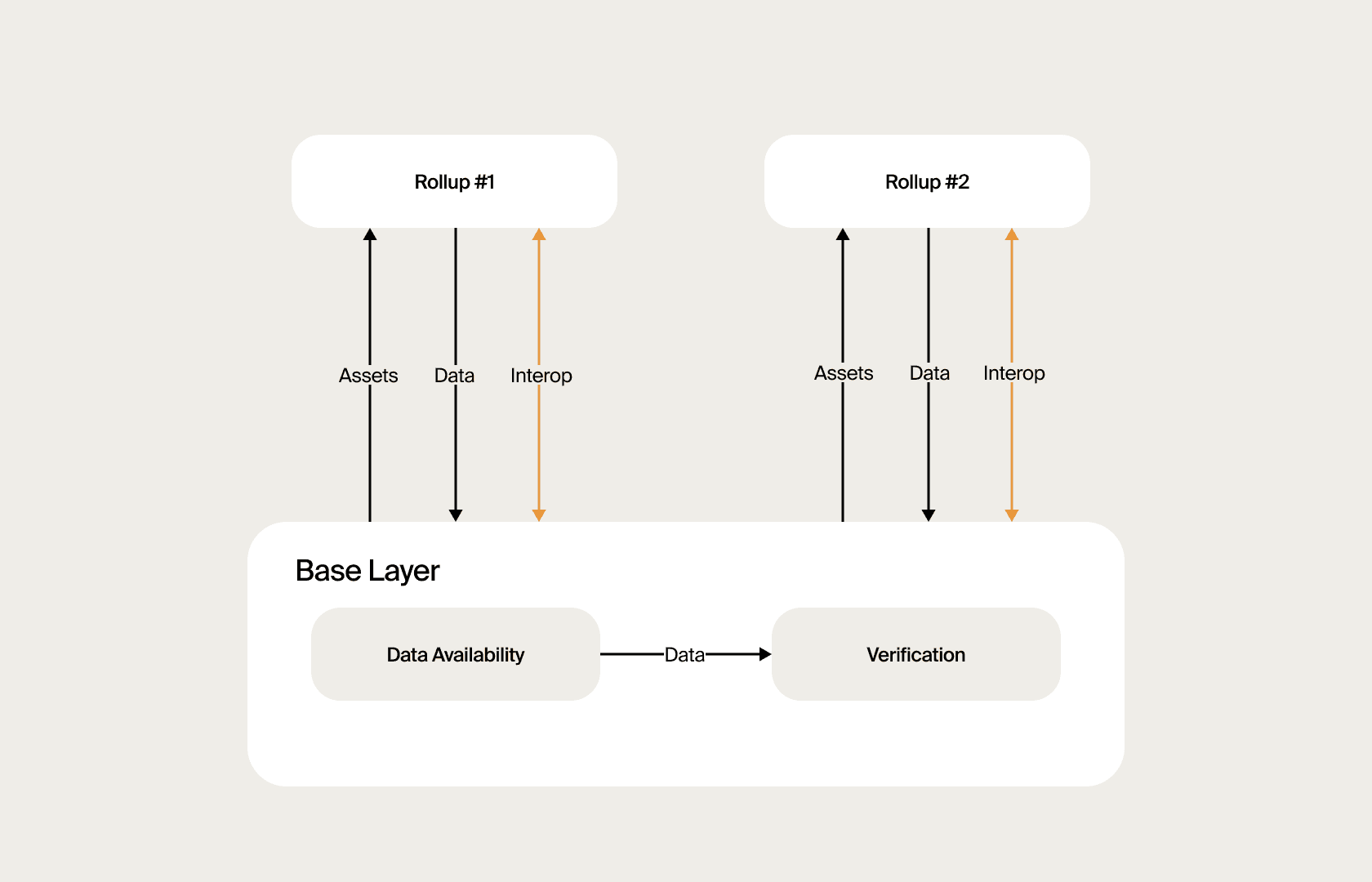

In the modular architecture, rollups maintain their own blockchain and build their own blocks using a centralized block producer (called a sequencer in rollup parlance). These blocks are accompanied by proofs. The proofs along with the rollup blockchain state are posted to the “base layer” i.e. Ethereum. Upon posting, these proofs are verified by all the nodes of the base layer. This allows the bulk of the computation to happen in a centralized way, but verification to happen in a decentralized manner. Links: Vitalik’s Endgame.

The overall system looks something like this:

Note: In the above diagram data is posted to a Data Availability Layer to make proof verification possible. The base layer effectively does the job of both the DA Layer and the Verification Layer

The rollup architecture is the right architecture as it allows applications to build out centralized but verifiable financial products tailored to their needs. However, we believe Bitcoin is just as good of a base layer if not better than Ethereum to host these apps:

Bitcoin commands over 50% of crypto market capitalization, making it the asset that most users want to utilize trustlessly. Only a rollup built with bitcoin as the base can achieve this. If the largest value proposition of base chains is to provide liquidity to apps built on top and be “money", BTC provides that as the largest asset in crypto.

Bitcoin will not attempt to compete with offchain domains building on top of it due to the relative ossification of the protocol. Ethereum is going to.

Proof-of-Work (PoW) might inherently be a better consensus algorithm for a decentralized base chain than Proof-of-Stake (PoS).

Bitcoin is now accepted by traditional finance as a store of value. No other asset in recent history has achieved this.

We expand on each of these points in this doc so as to not clutter things here.

Why Asula?

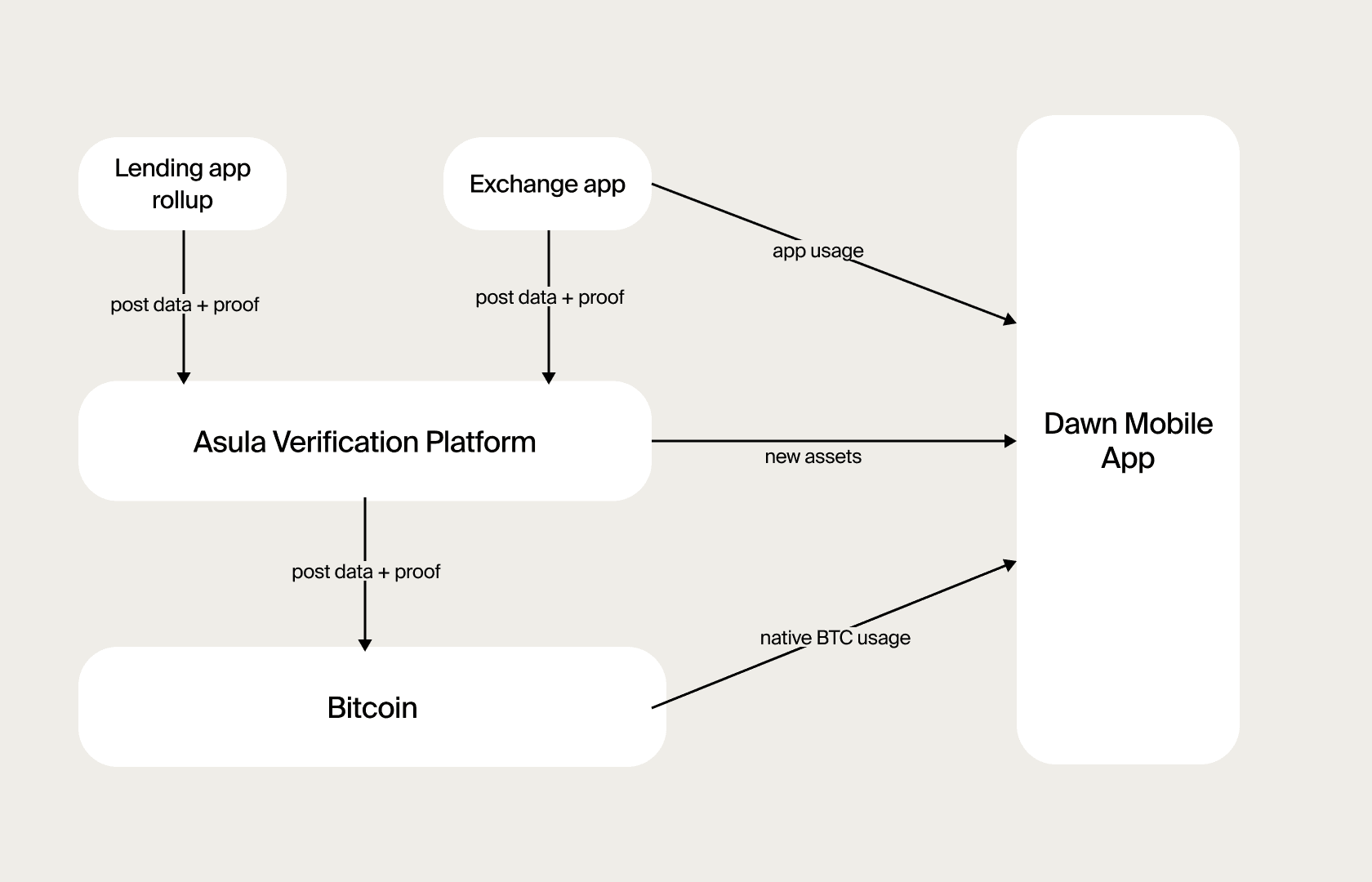

Our team is building software that uses knowledge across bitcoin, blockchain infrastructure and finance. In the end-state we plan to offer offchain domains that are built on Bitcoin, financial apps built on top of these domains and an interface to access them:

In the above architecture:

Dawn: Our wallet acts as an interface to access all blockchains and apps in our ecosystem.

Bitcoin: Maximally decentralized verification platform that verifies proofs posted by the Asula Verification Platform

Asula Verification Platform: Used to verify proofs from rollups built on top of it as well as to issue new assets. We need the AVP for the following reasons:

Proof verification on Bitcoin is going to be very expensive and slow (bitcoin has 10 minute block times and probabilistic finality). But for users to trust rollups, and for rollups to interoperate (transfer assets) with each other, there needs to be a faster and cheaper root of trust. AVP offers an intermediate root of trust before proofs are eventually posted to Bitcoin.

Bitcoin consensus also doesn’t recognize new assets. So assets would need to be issued on AVP as the root of trust. If assets were issued on each rollup individually, each team would need to go and partner with Circle for USDC or Tether for USDT replicating work. Large and common assets can be issued on AVP for all rollups to use easily. Since AVP would be faster than the 60 minutes it takes Bitcoin transactions to confirm, it will act as a decentralized middleman between different apps that don’t trust each other.

Apps: Apps are the most important part of the equation. Users want to be able to carry out financial activities without friction or the fear of losing their funds. We expect apps like lending + trading to be the dominant types of applications. The secret sauce for most of these apps will be in taking these primitives and tailoring it to their own use case (for example, StockX and the Nasdaq are both exchanges but serve very different kinds of markets and thus have different fee structures, interfaces, liquidity profiles etc).

(Note: some longer form discussion on our choice of this architecture can be accessed here)

Building out all of this today would be far too complex and would not be the most efficient way to test out demand. So we are focusing on building out a wallet and a lending protocol today:

Dawn will be our bitcoin+stablecoin focused wallet, which will effectively turn into a Bitcoin super app as we add features.

A lending protocol that allows us to create an MVP application which we can upgrade to the full architecture as defined above.

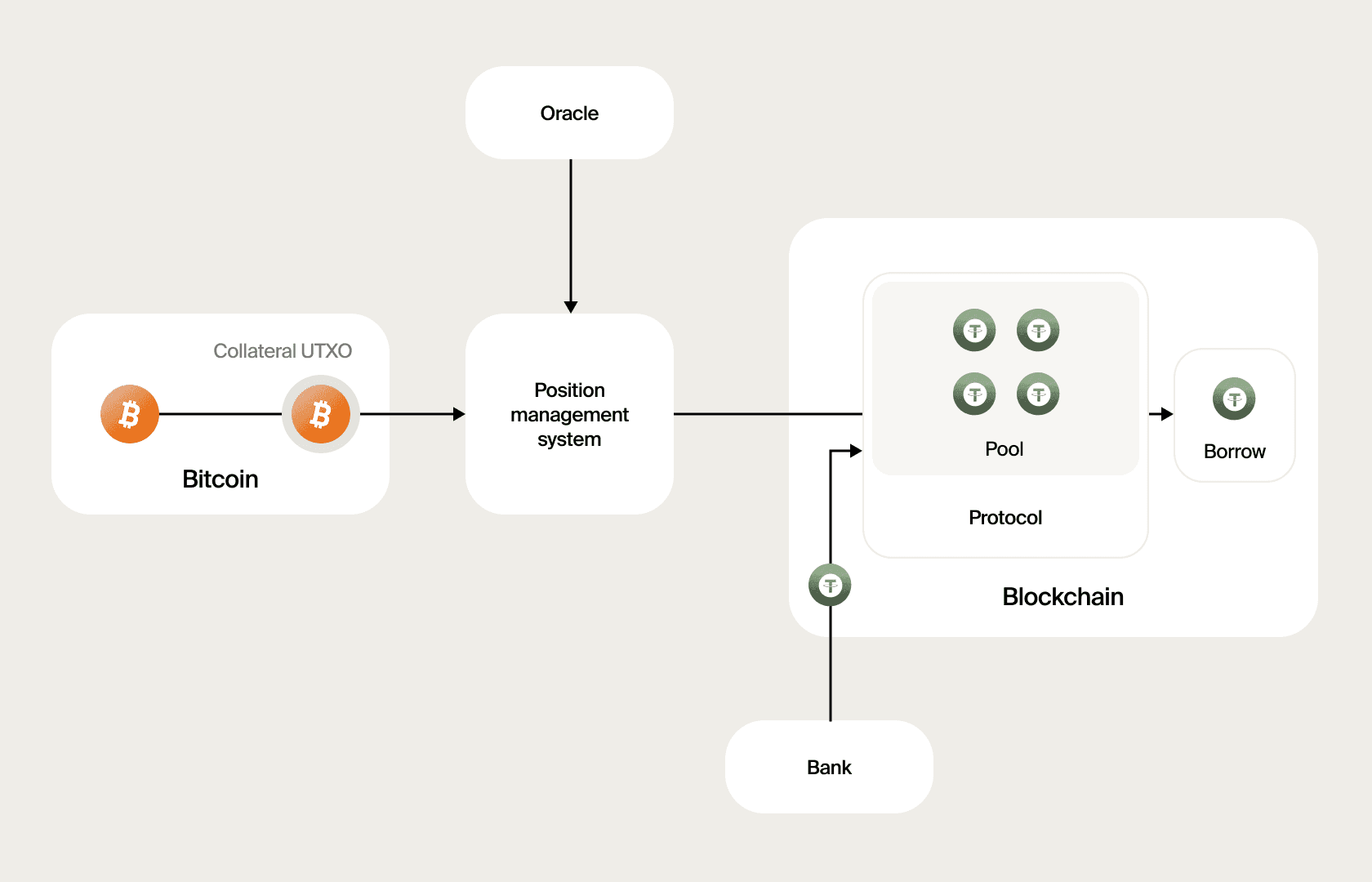

For more on Dawn feel free to read our product spec here, the lending protocol will follow system 3 from our blogpost here. We've attached the system diagram from the blogpost on lending below:

Why Crypto?

While we expect most of our readers to be sold on the idea of why crypto, we wanted to write a short section for posterity for anyone who isn’t.

Crypto provides the capacity for humans to have state-abstracted money and finance for the first time in history. Imagine if every country had to implement their own internet or their own search engine. The growth of every country would be dictated by the state of its education system and prevailing economic conditions. This would increase the knowledge gap between developed and developing nations. This is precisely what is happening when it comes to wealth. Being forced to hold currencies that represent the competence of their native governments has caused billions of people to lose large amounts of their buying power over the last decade and a half, a period during which Bitcoin’s market cap has grown from $0 to over $1,000,000,000,000. Bitcoin and crypto provide government-abstracted stores of value which can be self-custodied and rely on global consensus and decentralized networks to maintain their value. The value of cryptoassets like Bitcoin cannot be completely wiped out due to governmental policy in any one country in the world. Access to state-abstracted money for everyone seems like a worthwhile goal.

Even for offchain, real world assets, crypto is extremely useful. While all real world assets create trust assumptions in the custodian, putting real world assets on crypto rails allows us to enable two counterparties to settle trades between themselves without waiting for a trusted third party to look over or execute legal paperwork. This should dramatically increase the speed at which transactions can happen, reduce costs of doing business and generally increase the pace at which money moves, in turn, having a material impact on the GDPs of countries that adopt crypto rails. Features such as permissionless/trustless vaults, escrows, instant settlement, liquidity aggregation on exchanges and lending markets, privacy-preserving trading via dark pools are all features unique to blockchains.

© 2025 Asula